ajoknoblauch

Registered

- Joined

- Feb 21, 2013

- Messages

- 6,358

- Likes

- 3,909

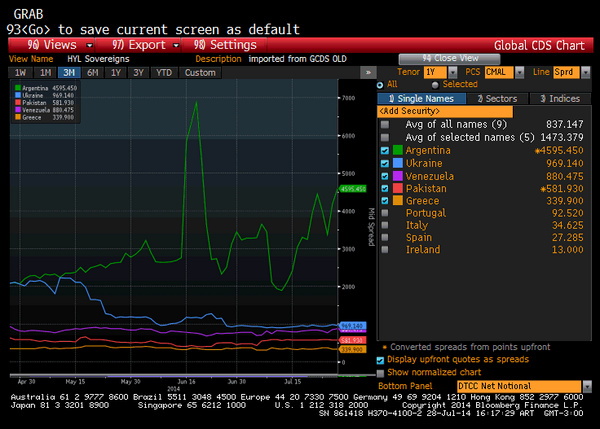

If the Argentine Republic does not pay it's bondholders (including the holdouts - Buitres) by this Wednesday in accordance to US Judge Griesa the Republic will default. Many US papers are reporting this as a belligerent Argentina refusing to pay it's debts, again. However, that is far from the whole story and, I think, quite simply inaccurate.

The Republic is arguing that it cannot legally negotiate with the holdouts because that would trigger the RUFO clause. This clause prevents The Republic from offering a better deal to the holdouts than they offered originally to the bondholders who accepted the new payout terms. In other words, if Argentina pays more to the holdouts than they pay the other bondholders then they can be taken to court for violating the terms of the agreement. That could be Billions of Dollars at stake.

But ... if The Republic does not pay according the court order it will default. If The Republic defaults that will trigger acceleration clauses in all of it's foreign law bonds. That risks court action in multiple jurisdictions and Billions of Dollars at stake.

This could be a decision of the lesser of the two evils which, at this point, appears to be to default.

What's a good Republic to do? What do you think will happen on/or by Wednesday?

GS

Whar "good Republic" is involved in this?

I just know that the CC bill will be not only charged with the 35% but with a hefty exchange difference on the bill witch will arrive next month!

I just know that the CC bill will be not only charged with the 35% but with a hefty exchange difference on the bill witch will arrive next month!